The third gloomy quarter for Article 9 funds

The Sustainable Finance Disclosure Regulation (SFDR), introduced by the European Union in March 2021, represents a significant milestone in sustainable finance regulation. The framework categorizes investment funds into three distinct classifications: Article 6 (no sustainability integration), Article 8 (promoting environmental or social characteristics), Article 9 (having sustainable investment as its objective).

Initially heralded as a game-changing transparency tool, SFDR aimed to combat greenwashing and provide clarity to investors.

The regulation’s evolution has been marked by several key phases. In its early implementation, many asset managers rushed to classify their funds as Article 9, seeing it as a prestigious label. However, by late 2022, regulatory scrutiny intensified, leading to a wave of downgrades from Article 9 to Article 8 status. This “downgrade wave” highlighted the challenges in meeting the stringent requirements of Article 9 classification, which demands that all investments, except those for specific purposes like hedging, must have sustainable objectives.

The regulatory landscape continued to evolve with the introduction of additional technical standards in January 2023, requiring more detailed disclosures about environmental and social impacts. These changes have forced asset managers to be more precise and cautious in their fund classifications, leading to a more mature but arguably more conservative approach to sustainable investment labeling.

Despite growing awareness of climate risks and ESG concerns, these supposedly elite sustainable investment vehicles are facing significant outflows. This situation has left many industry observers scratching their heads. Article 9 funds have just experienced their third consecutive quarter of withdrawals, with a record-breaking outflow of €6.2 billion in Q2 2024. The only one asset class within Article 9 managed to stay afloat was fixed income, pulling in €4.22 billion in 2024 (Morningstar).

What’s behind this shift in investment interest?

What does it mean for the future of sustainable investing?

What are some possible ways to boost the confidence of sustainable investors?

This article attempts to shed some light onto the currently gloomy scene of sustainable investing.

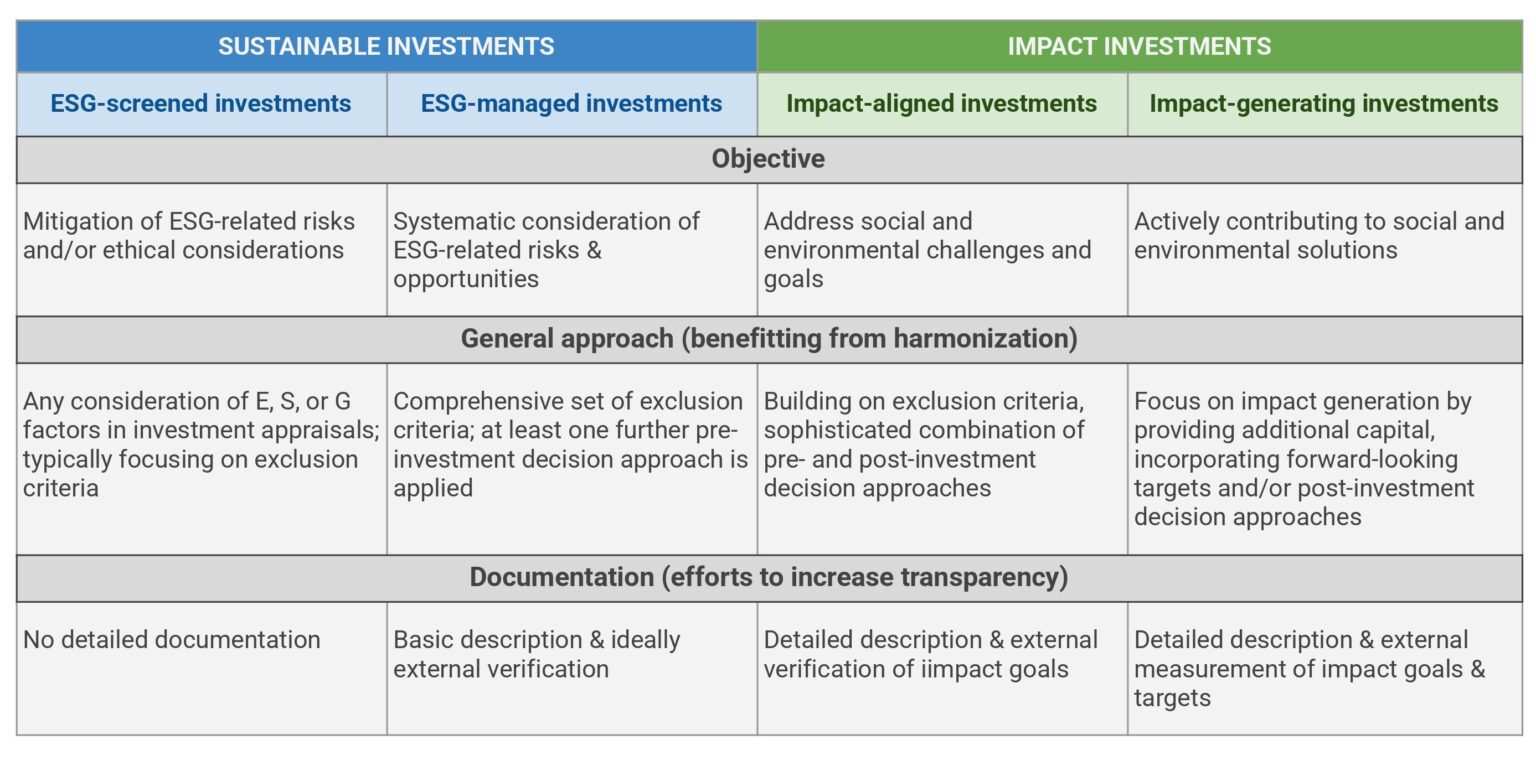

Does sustainable investment objective equal impact?

One of the primary issues plaguing Article 9 funds is the disconnect between their stated objectives and demonstrable impact. While a staggering 72% of these funds claim to have impact-generating objectives in their product documents, only a mere 20% can actually demonstrate how their investment strategies contribute to tangible environmental or social outcomes (Scheitza et al.). This disparity has led to growing skepticism among investors and calls for greater accountability in the sustainable investment sector.

Adding to the confusion is the interchangeable use of terms like “impact investing” and “Article 9 Funds”. Industry experts warn that this conflation is not only inaccurate but potentially misleading. The reality is that funds classified under Article 9 encompass a broad spectrum of investments, including both impact-related and ESG-related strategies. This ambiguity is largely due to the discretion allowed by the SFDR in defining and implementing sustainable investment objectives.

Perhaps most concerning is the misuse of the SFDR itself. Originally introduced as a transparency regulation, the EU Commission has explicitly stated that it was never intended to serve as a labeling regime. However, many financial market practitioners have seized upon the Article 9 classification as a marketing tool, prominently featuring it in promotional materials. This practice not only contradicts the regulation’s intended purpose but also contributes to the growing confusion among investors.

As the sustainable investment landscape continues to evolve, it’s clear that greater clarity and standardization are needed. Investors deserve transparency and concrete evidence of impact when entrusting their capital to Article 9 funds. Only by addressing these challenges head-on can the industry restore confidence and ensure that sustainable investing truly lives up to its promise of creating positive change in the world.

Does impact investing equal lower financial returns?

When it comes to impact investing, a common misconception is that doing good for the world means sacrificing financial returns. However, recent findings challenge this notion, revealing a more nuanced picture of the risk-return profile of impact funds. Contrary to popular belief, impact investing actually demonstrates lower exposure to market risk compared to other private market strategies. This intriguing characteristic not only supports the hedging view of ESG but also suggests that impact investing can be a valuable tool for portfolio diversification (Jeffers et al.).

Diving deeper into the numbers, Jeffers et al. find that impact funds are less sensitive to public equity market movements than their traditional counterparts, including venture capital funds. This reduced market sensitivity could be a game-changer for investors looking to shield their portfolios from market volatility. While it’s true that impact funds may show lower total returns compared to benchmark non-impact funds, the gap narrows significantly when market risk exposure is taken into account. For investors who prioritize risk-adjusted returns, this revelation positions impact funds as a compelling option that doesn’t necessarily require sacrificing financial performance for social and environmental benefits. As the investment landscape continues to evolve, these insights invite us to reconsider the role of impact investing in modern portfolio management.

Impact investors should leverage non-financial strategies to generate impact

In the ever-evolving landscape of sustainable finance, impact investing has emerged as a beacon of hope for those seeking to align their financial goals with positive societal change. However, as the sector grows, so do the challenges and skepticism surrounding its effectiveness. Experts are increasingly questioning the ability of impact funds to deliver on their promises, raising concerns about mission drift and “impact washing”.

Recent studies suggest that impact funds need to go beyond simply providing financial capital and focus on adding value through non-financial support. This approach mirrors the strategies of traditional venture capitalists, with impact funds engaging in services related to process optimization, human resources, marketing, communications, and network access (Nachyła et al.).

So, how exactly should impact funds leverage these non-financial strategies?

At Impact Labs, we believe that the implementation should occur in three folds.

Investee Level

Impact funds should roll up their sleeves and get hands-on with their investees.

This includes helping companies plan and model their environmental and social impact, measure it, integrate it into their business models, and report it to stakeholders. At the same time, negative externalities should also be taken into consideration where preventative measures and policy should be incorporated into the business strategy. Organizational learning should also be implemented on a continuous basis to make sure that all stakeholders are aligned on the same vision.

Client Case Example:

- Partnered to develop an impact roadmap aligned with global sustainability goals.

- Integrated environmental metrics into business strategies for measurable outcomes.

- Positioned as a future leader in the sustainable chemistry sector.

Read our client case

BIOMANITY

Building a Path Toward Green Chemistry Leadership

Fund Level

The impact shouldn’t stop at the investee level.

Within the funds themselves, managers should design impact-driven clauses, policies, and processes. This includes everything from legal and governance matters to talent management and carried interest structures. Setting up funds KPIs with an outside advisory committee and LPs would also ensure the fund managers’ commitment towards impact. Regular workshops and trainings for all stakeholders within the fund is also necessary to make sure everyone’s vision is aligned.

Client Case Example:

- Conducted tailored ESG and sustainability workshops for fund managers.

- Introduced double materiality analysis to guide strategic decision-making.

- Developed frameworks for impact-driven policies and governance structures.

Client case coming soon

SOUTH

Embedding Impact in Fund Management

Community Level

Impact funds should foster collaborations among investees and connecting them with other stakeholders.

It’s like creating a sustainability ecosystem where the whole is greater than the sum of its parts. Discussions among like-minded individuals would foster growth and often sparks new ideas.

By embracing these multi-faceted strategies, impact funds are not only addressing concerns about their effectiveness but also paving the way for a more robust and impactful investment landscape.

As the sector continues to evolve, it’s clear that the future of impact investing lies not just in the size of the check, but in the depth of engagement and the breadth of value and impact creation.

References

Scheitza, Lisa, and Timo Busch. “SFDR Article 9: Is it all about impact?.” Finance Research Letters 62 (2024): 105179.

Jeffers, Jessica, Tianshu Lyu, and Kelly Posenau. “The risk and return of impact investing funds.” Journal of Financial Economics 161 (2024): 103928.

Nachyła, Pola, and Rachida Justo. “How do impact investors leverage non-financial strategies to create value? An impact-oriented value framework.” Journal of Business Venturing Insights 21 (2024): e00435.

Taskforce, Impact. “Financing a better world requires impact transparency, integrity and harmonisation.” 2021,